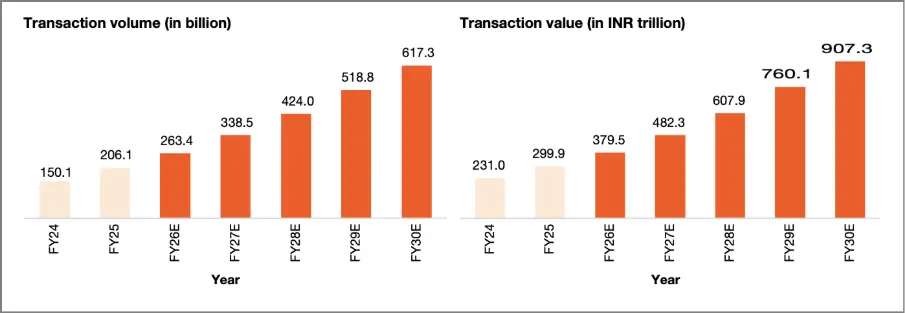

Digital payments in India, led by Unified Payments Interface, are growing at an exceptional pace. Transaction values continue to rise year after year, reflecting how deeply digital payments are now part of everyday life. The graph below highlights this momentum, with transaction volumes growing YoY and an expected 300% increase in both transaction volume and rupee value by FY30 vs FY25.

Emerging Trends:

- UPI payments are the key driver of this growth – with its ecosystem of participating Banks (~700), merchant ecosystem (~65 million) and serving nearly half a billion customers. UPI in terms of Volumes is expected to grow contribute ~85% in terms of rupee value of all digital payments by FY30. Add to this the 40 authorised TPAPs, the ecosystem is bound to flourish and is also insulated from external threats (eg. GPay, visa, mastercard shutting down in Russia); given that this is completely Made in India tech stack.

A key component of UPI Payments is the Merchant Eco System – currently contributing ~30% of current value to ~63% in terms of Rupee value.

- Debit and Credit Cards comprising POS and Digital spends, expected to grow at a CAGR of 25%, with spends primarily coming from credit cards and increase penetration of UPI linked credit cards. The spends growth will be primarily driven by digital spends which is expected to be around 72-75% (FY30) from the current 63%. – this represents a a perceptible shift away from the traditional Brick and Mortar Merchant.

- Prepaid / Fastag & SI transactions is expected to see a steady growth with primary spends being digital in nature.

- Emergence of Fintechs, TPAPs, Payment Banks, Telcos once dominated primarily by banks and technology firms, the sector now attracts players from diverse fields such as retail, telecommunications, FinTech, and e-commerce, enabling cross-sector innovation and new market entrants.

The above trends is a paradigm shift vis a vis what we have seen till a few years ago and brings with it, its own perils such as cybercrime and fraud risks. Cybercrime has evolved to such and extent that FY25 has seen a 24% spike in cybercrimes reported on the NCRP portal, with the rupee value of reported fraud loss being INR 22,495 crores. This is the reported numbers and the overall non reported instances could be approximated to be 1x in terms of rupee value. Given that this is majorly digital, the merchant eco-system plays a key role in the same; payment instruments like VPAs, underlying merchant accounts etc are used extensively as collections accounts to receive the proceeds of such crime or act as an intermediary in the laundering of such proceeds.

Hence it is that much more imperative that there is a lot more focus on the kind of merchant who are being on boarded; given the digital nature of merchant spends and the ease at which the merchant can evolve post onboarding, a Life Cycle based Risk Management Approach is the need of the hour.

Every merchant you onboard is a vote of confidence in your platform. But every transaction they process is also a new surface for risk.

Hence, what starts at onboarding shouldn’t stop there; it needs continuous attention. In this blog, we will discover-

- How one-time checks are not enough in merchant onboarding

- How rapid growth in digital payments is increasing risk

- And how end-to-end merchant evaluation can make a real difference

How One Time Risk Checks are not Enough in Merchant Onboarding?

There is a traditional belief that all merchant risks can be tackled before onboarding and once the onboarding is completed, no merchant risks can travel, making the following, the key checkpoints of merchant onboarding –

- Verify business details

- Review website

- Approve and go live

But as the digital payment ecosystem is growing more complex, merchant risk monitoring does not stop at onboarding. Assuming that merchants will remain compliant after initial checks is often unreliable. In reality, risks can emerge at any stage post-onboarding, such as –

- Change in website content

- Sale of restricted / banned / high-risk products

- Manipulate redirects or hidden flows

- Drift away from declared business categories

All of this happens after onboarding, when visibility is often limited.

How Scaling Digital Payments Elevates Risk in Merchant Onboarding

While digital adoption is speeding up, it also brings in new risks that don’t just appear at the start, they continue throughout the merchant journey.

More merchants mean:

- More variation in quality and intent

- More edge cases that manual checks miss

- Higher probability of fraudulent or non-compliant entities slipping through

However, stopping the merchant ecosystem from evolving is not the solution- “Continuous Monitoring”, is.

Why Onboarding Checks Alone aren’t Enough & How Continuous Monitoring Fills the Gap?

Here’s how comprehensive and continuous merchant risk monitoring strengthens payment getaways, enabling them to fill the gaps created by just focusing on merchant onboarding – (also include business outcome)

| Onboarding-only monitoring limitations | How holistic monitoring helps |

|---|---|

| One-time snapshot of the merchant | Continuous tracking of merchant behavior |

| Misses post-onboarding risks | Detects emerging risks in real time |

| Relies on static documents | Validates ongoing digital presence and activity |

| No visibility into changes in offerings | Flags deviations in products/services |

| Cannot track compliance drift | Monitors policy compliance risk continuously |

| Misses malware or suspicious activity later | Scans regularly for threats and anomalies |

| Reactive issue resolution | Enables proactive risk prevention |

| Higher risk of regulatory/reputation impact | Strengthens against compliance risk and brand protection |

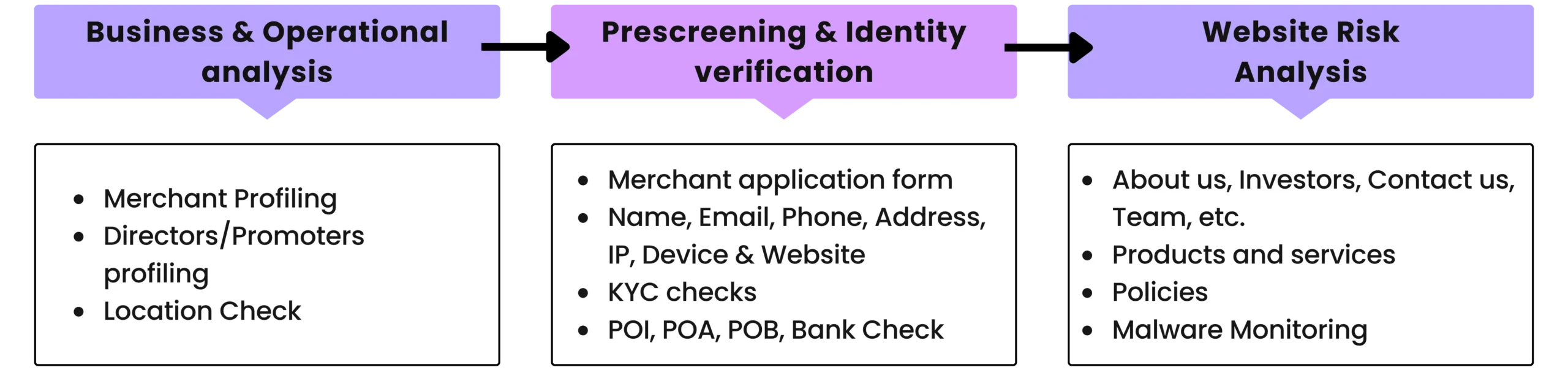

End-to-End Merchant Evaluation: A New Outlook to The Merchant Life Cycle.

Merchant onboarding now demands confidence that cannot be achieved without holistic evaluation of merchant lifecycle, one that goes beyond onboarding and keeps validating risk at every stage.

That’s where mFilterIt’s approach and product offerings steps I; not only focussing on onboarding but also monitors and evaluates risk which may evolve at a later stage.

Business & Operational Analysis

We help you truly understand who you’re onboarding by looking beyond basic details-analyzing the business, verifying promoters, and checking location authenticity.

Outcome: You onboard genuine, trustworthy merchants from the start.

Pre-screening & Identity Verification

We validate merchants using multiple signals like contact details, device, IP, and KYC documents to catch inconsistencies early.

Outcome: Lower chances of fraud and stronger defence against compliance risk from day one.

Website Risk Analysis (and beyond)

We continuously monitor the merchant’s digital presence-checking website content, offerings, compliance, and any suspicious activity.

Outcome: Early detection of risks and better control even after onboarding.

Overall impact: You move from one-time checks to continuous visibility—helping you build a safer and more reliable merchant ecosystem.

Conclusion

As digital payments continue to scale, relying on one-time onboarding checks is no longer enough. Continuous evaluation is what enables real control, stronger compliance, and long-term trust in your merchant ecosystem.

If you’re looking to move from reactive risk management to proactive oversight, it’s time to take the next step, schedule a demo with mFilterIt and see how continuous merchant risk monitoring can work for you.

FAQs

What are the risks that can occur after merchant onboarding?

Post-onboarding risks include changes in website content, introduction of restricted products, policy violations, suspicious redirects, malware activity, and deviation from declared business categories.

What is continuous merchant monitoring?

Continuous merchant monitoring is the process of regularly evaluating a merchant’s behavior, digital presence, compliance risk status, and risk signals even after onboarding, ensuring ongoing trust and safety.

What are the best practices for managing merchant risk?

Effective merchant risk management starts with continuous monitoring, strong verification processes, and proactive fraud prevention strategies. Businesses should regularly evaluate traffic sources, affiliate partners, payment activities, and customer behavior to identify suspicious patterns early.

What is the difference between onboarding checks and continuous monitoring?

Onboarding checks provide a one-time snapshot, while continuous monitoring tracks changes over time, detects new risks, and ensures ongoing compliance.